Long term care insurance is relatively new to Canada and not generally well understood. I met Travis Attlebery, a Health & Life Insurance Advisor with Laurentian Financial Services, at a health fair. He is one of the only people I ever thought I would trust to buy insurance from. He gave me these answers to questions I asked him about long term care insurance. Contact information for Travis follows the end of the article below.

1. What Other Sources of Income Might Be Available to me? Do I need to protect my income?

Determining how much Long Term Care Insurance (if any) is needed is not an exact science. There are four future assumptions that need to be made:

- How much will the care program cost?

- How much passive income will you have?

- How will your other expenses change?

- What will inflation be?

Let’s say Mrs. Smith anticipates needing $5,000 per month for a care program in 10 years. She anticipates having a fixed income of $2,000 per month, of which $1,000 goes to fixed expenses. In this case, there is a shortfall of $4,000 per month. This is the amount of Long Term Care Insurance that should be purchased.

This is a very simple demonstration of the process. Please keep in mind any assumptions about the future are just that: assumptions. Nobody has a crystal ball. Long Term Care Insurance should be part of your overall financial plan, which should be reviewed annually.

2. Why am I saving my money?

Setting your personal financial goals is the foundation of any financial plan. The point of a financial plan is to help you realize those goals. Only you can decide what you want to spend your money on.

Setting your personal financial goals is the foundation of any financial plan. The point of a financial plan is to help you realize those goals. Only you can decide what you want to spend your money on.

If you believe that money should be set aside for long term care, long term care insurance is a great way to provide for that need. There are really only two sources to draw from for long term care: savings or an insurance policy.

There are two examples below that illustrate how you might save. They are based on a Long Term Care Insurance Policy that pays benefits for five years. You may need more time, however. You can buy insurance for longer term payouts, but the premiums are higher.

Example 1:

Savings

Figure 1 shows how saving $90 per month will grow at 8%. The blue columns are savings in a taxable account* and the red columns represent savings inside a tax deferred account such as an RRSP.

As you can see, even in a tax deferred account it would take over 30 years to save $120,000 after taxes. This is the value of the insurance policy illustrated below.

Figure 1

*The above figure assumes an 8% before tax return and a tax rate of 21.05%. The RRSP calculations are before tax.

Insurance

A long term care contract for a 60 year old male living in British Columbia would have a monthly premium of about $90 per month**. The contract would pay a tax free monthly benefit of $2,000 per month for 5 years. This represents a total value of $120,000 ($2,000 X 12 X 5). With an insurance contract, that money is available immediately if you qualify for a claim.

There are risks associated with both the savings and insurance approaches. The savings approach poses the danger that you require long term care before you have saved enough money to cover the costs. Of course, the risk with the insurance approach is that you don’t require long term care and you never file a claim. Which risk you wish to assume will depend on your unique circumstances.

**The contract illustrated here is the Desjardins “Independent Living” plan with a monthly benefit of $2,000 per month and a 90 day waiting period. It is for information purposes only and should not be considered a recommendation. Consult with a licensed Life Insurance Advisor before purchasing any long term care insurance.

Example 2:

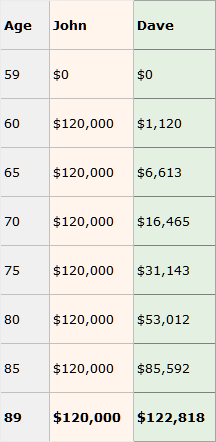

Let’s look at John and Dave (both aged 60) and their different approaches.

John purchased a long term care contract** with a monthly tax free benefit of $2,000 for 5 years. His premium is just under $90 per month. If John qualifies for a claim, that money becomes available to him after his selected waiting period is over. The total value of John’s contract is ($2,000 per month X 5 years) $120,000.

Dave, on the other hand, decided to take that $90 per month and invest it. Dave invests wisely and averages an 8% return. To makes things even better, Dave pays no tax on his investments! Here is how the two approaches compare:

Money Available for Long Term Care

Of course, if Dave had to pay taxes on his investments, it would take considerably longer for him to match John.

**The contract illustrated here is the Desjardins “Independent Living” plan with a monthly benefit of $2,000 per month and a 90 day waiting period. It is for information purposes only and should not be considered a recommendation. Consult with a licensed Life Insurance Advisor before purchasing any long term care insurance.

3. When does it “kick in? What will trigger it?”

Every contract is different and should be read carefully. The usual basis for claim under a long term care contract is the inability of the insured to perform two of the six Activities of Daily Living (bathing, dressing, eating, transferring, toileting and maintaining continence) or cognitive impairment. Once the insured satisfies either of these conditions, a claim can be made.

4. When and how are benefits paid out?

There are two types of long term care contracts: income and reimbursement. The income plans work like an annuity. After the claim has been approved a monthly payment is made to the owner of the contract. There are no restrictions on how the money is spent.

The reimbursement plans will reimburse the owner of the contract for approved expenses. When purchasing such a contract it is important to know which expenses are covered and which are not. For example, it is quite common to not allow payments to family members even if they are qualified to provide care.

5. What are payment methods and options? How do they compare across packages?

Premiums can usually be paid monthly, quarterly, semi-annually or annually. As a rule, annual payments are more economical than monthly payments as there is a service fee charged for the convenience of monthly payments.

Premiums will depend on the length of the waiting period, the length of coverage chosen, the age, sex and health of the insured. It can be quite difficult to compare contracts on an “apples to apples” basis as some companies pay a daily benefit, others monthly. There will also be advantages and conditions unique to each company. A brief overview of some of the leading companies follows the question and answer portion of this article.

6. What conditions are not covered?

Each contract is different and should be read carefully. Some standard exclusions and limitations are: attempted suicide, self-inflicted injury, and nervous or mental disorders without proven organic cause.

7. What does it cover? Nursing Homes? Assisted Living? Home Care? Rehabilitation Services?

This is an important consideration when purchasing a reimbursement plan. Some plans are limited to facility care, while others have broader coverage. There are generally no restrictions on income plans. As most people want to stay in their own homes, it is important to consider whether the plan will cover support services in the home, or equipment that you might have to buy to stay in your own home.

8. Can my premiums go up?

Premiums are generally guaranteed for 5 years. After that, they may be increased as a class (meaning premiums for a group are increased). An increase in premiums for existing policyholders must receive government approval and happens only rarely. The risk of increasing premiums is there and should be taken into consideration.

9. Are costs of services covered by inflation

There are inflation protection riders available for most products. These should be looked at carefully as there are often maximum annual percentage increases and the benefits are usually linked to the Consumer Price Index (CPI). However, over the last 5 years the cost of Health Care Services has risen 50% faster than the CPI as a whole.

As for the inflation question, that’s one of the biggest obstacles to financial planning. It’s a complete unknown and the best approach is to make sure your savings are invested in “inflation beating” investments. If you rely on the inflation protection rider entirely, there could be a serious difference between costs and benefits.

10. Is there a waiting period before I can access benefits?

Much like you can choose the deductible on your home insurance, you can choose the waiting period (sometimes referred to as elimination period) for long term care insurance. Depending on the policy, it can range from 0 to 180 days. The longer the waiting period, the lower the premiums are because you are assuming more of the risk and the insurance company is assuming less risk.

11. Other restrictions on accessing and using the benefits?

Some policies only cover facility care or other “approved” expenses. When choosing a long term care insurance contract it is imperative to ascertain what is covered and what is not before signing anything.

12. How much coverage will I get per day/month/year?

Your Health & Life Insurance Advisor should do a thorough analysis to determine how much coverage you need. When you purchase the coverage the contract will clearly state the amount per day/month of the benefit. Take a look around at what services cost now—a homemaker or companion in 2006 is close to $20.00 per hour, for a minimum of two hours. If you will need five hours of help a day, that is $100.00 per day, or $3,000. per month—at today’s prices! What will inflation make those services costs in ten years when you need them? That is what you want the policy to cover.

13. Are there limits to the benefits?

Yes. There will be a specific term stated in the contract. The term of coverage chosen can range from 2 years to lifetime coverage. The length of the contract will have a significant effect on the premiums—the longer the payout period, the higher the premium.

14. Can you start and stop receiving payment, if you get ill, improve, then become ill again?

Yes. Most contracts will outline under which conditions payments stop and start.

When do premium payments stop?

Premiums will generally cease when benefits are being paid out. There are some contracts available that limit how long premiums must be paid for. However, every contract is different and this should be considered on a case by case basis.

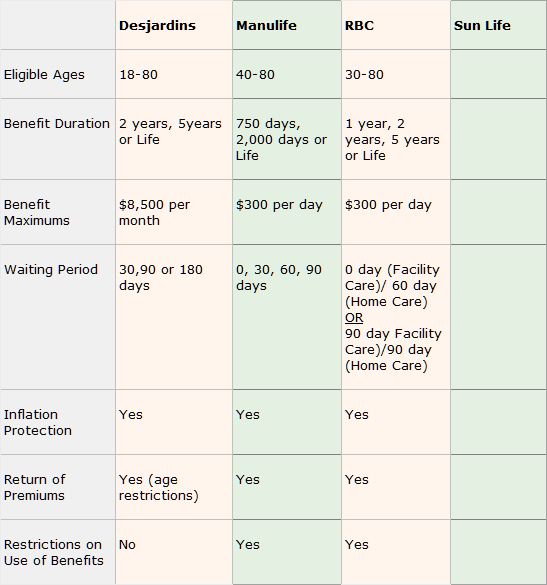

There are four large insurance companies that offer long term care insurance in Canada right now. Below is a brief overview of the contracts that they offer. However, you should consult with a licensed Health & Life Insurance Advisor before entering into any contract. The following is for information only and in no way should be considered advice or an endorsement of any of the products.

You can contact Travis at http://www.lfsvancouver.com/ or

LFS Laurentian Financial Services

and Optifund Investments Inc.

200-13737 72nd Avenue

Surrey BC, V3W 2P2

604.592.2360